Unlock Your Financial Potential with Advanced Debt Consolidation Calculators Discover the Transformative Power of Debt Consolidation Calculators for Your Financial Well-Being Debt consolidation calculators serve as essential financial tools designed to help individuals gauge their potential debt consolidation savings. By utilizing these calculators, users can conduct in-depth analyses that juxtapose their existing debt obligations against…

Debt Consolidation Tips for Single Parents

Empowering Single Parents: Inspiring Narratives of Debt Consolidation for Achieving Financial Independence Transformational Journeys: Real-Life Accounts of Financial Empowerment For single parents grappling with the overwhelming task of managing their debt, the path toward debt consolidation can often feel intimidating. However, numerous individuals have embarked on transformative journeys toward financial freedom, sharing compelling stories that…

Smart Money Management Strategies To Avoid Reliance On Loans

As the old saying goes, “money doesn’t grow on trees.” And for many of us, it can feel like no matter how hard we work or how much we save, there’s never quite enough to go around. In times of financial stress, it can be tempting to rely on personal loans as a quick fix…

23 Better Money Habits You Need to Start Doing in 2022

23 Better Money Habits You Need to Start Doing in 2022: One step at a time and adopting better money habits can help you take control of your finances to start building a brighter future for yourself. It’s possible that terrible money habits are to blame if you have trouble saving for the future or…

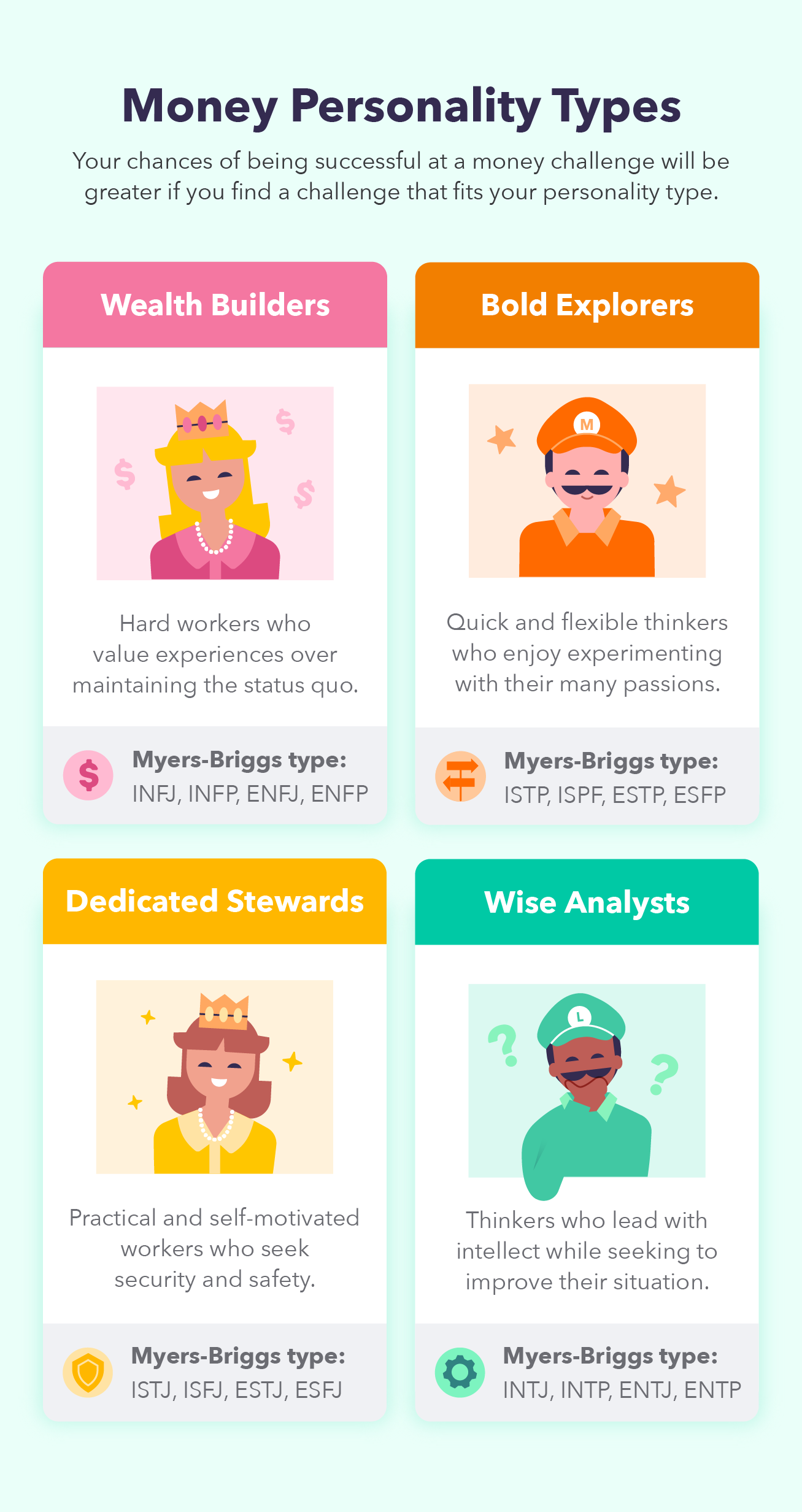

Money-Saving Challenge: 30 Types For Every Personality in 2022

Money-Saving Challenge: 30 Types For Every Personality in 2022: There are many budgeting strategies to choose from when it comes to saving money, whether it’s for a short-term goal, such as a trip, or a long-term goal, such as a retirement fund. Starting a money-saving challenge can be a good way to save money while…